Editor’s Note: This post has been updated with new information.

Your credit score plays a big role in your overall finances. We talk a lot about What goes into a credit score? and how can you keep it in top formBut where do your scores actually come from?

Let’s take a look at the three main credit reporting agencies that determine your score.

New to The Points Guy? Registration for our daily newsletter and check our beginner’s guide.

3 main credit reporting agencies

There are three main credit reporting agencies that collect your financial information and compile it into a report – TransUnion, Equifax, and Experian. Those reports are an important part of your credit score, and it’s what banks and creditors collect when you apply for a credit card, loan, or other line of credit.

Each credit reporting agency has its own method for compiling your credit report and determine your credit score. That’s why your score can vary from agency to agency. Let’s take a look at each agency and the score each agency generates. Then we’ll talk about which issuers consider which scores when you apply for a new card.

TransUnion

TransUnion was founded in 1968 as the parent company of the Union Tank Car Company (a railcar rental operation). The company jumped into the credit reporting business in 1969 when it acquired the Cook County Credit Bureau (CBCC). Since then, it has expanded its services beyond credit reporting. But it is still one of the main credit bureaus in the country.

One of the defining characteristics of TransUnion is that it provides a service called Identity Key. If you believe you are a victim of identity theft, TransUnion will place freeze on your report And contact Experian and Equifax to let them know about the freeze.

vehicle

Equifax is a global data, analytics and technology company. Like TransUnion, it is another major credit reporting agency used by lenders, although it also offers other financial services. Equifax has been in the spotlight for the past few years after big data breach was reported in September 2017 affecting 147 million people. In the years since, the company committed to security transformationHire new leadership and take steps to rebuild its reputation and security infrastructure.

Sign up for our daily newsletter

experience

The last of the “three adults” was Experian. I realize that Experian has a lot more to offer in terms of credit education. It issues multiple reports each year based on data and analysis collected by the company. Of course, Experian also offers credit monitoring and reporting services.

The company now known as Experian actually started as a London-based forum in 1803. But the US credit reporting business actually started under the company name TRW, which acquired Data credit data (a credit reporting agency) in 1968. Eventually, London and the United States companies merged to form Experian, the global company it is today.

Related: How to check your credit score for free

FICO vs. VantageScore

FICO and VantageScore are the two main methods that credit reporting agencies use to determine credit scores. All three methods are used by all three agencies to determine different types of scores. FICO is the older method and has been around much longer. VantageScore is newer, developed by all three major credit reporting agencies in 2006.

Both grades range from 300 to 850 — higher score, the more reliable the borrower is considered. Although there is much overlap in the factors that each method considers, there are some slight differences between the two methods.

FICO gives specific percentages for each factor:

- Payment history (35%).

- Amount owed (30%).

- Length of credit history (15%).

- New credit (10%).

- Credit mix (10%).

VantageScore keeps its formula in the vague side, listing the overall importance of each factor:

- Payment history (hugely impactful)

- Age and type of credit (highly influential)

- Rate of credit line used (highly influential)

- Total balance and debt (moderate effect)

- Recent credit behavior and inquiries (less impact)

- Available credit (less impact)

There is no single credit score used by every credit card issuer, bank, and lender. In addition, each credit reporting agency may have different financial information on file. Unfortunately, this may mean you odds for approval varies depending on what type of score is used to make the decision.

Related: Your FICO score and which credit issuers offer it for free

Which credit bureau does the bank check?

When you credit card registration, the issuer contacts (or several) credit bureaus to purchase a copy of your credit report. Included in your report are the categories mentioned above. Knowing which credit reporting agency the card issuer uses to get the report can give you a better idea of your approval rate.

You can also use this knowledge to free up your apps (or combine them, as the case may be) in a way that helps you maintain Optimal credit scoreeven if you sign up for more cards in a shorter time frame.

Many credit card companies tend to rely on an office when they process credit card app. However, the credit bureau they use to purchase reports can vary depending on the state you live in and the specific card you want.

Here are a few anecdotal data points that have been reported over the years:

- city usually get credit reports from Equifax or Experian.

- Amex mainly pulls Experian, although sometimes reports Equifax or TransUnion.

- Chase endorsing Experian, but can also purchase Equifax or TransUnion reports.

- capital one no favorites – but often drag more than one.

Let’s say you find out that Citi usually gets from Equifax and Chase mainly uses Experian. You can apply for a card from both issuers in one day and potentially improve your approval rate for both.

Unfortunately, credit card companies do not publicly disclose which credit bureaus they endorse. However, there are online sources that collect customer feedback to provide an overall average of which credit bureaus the issuer uses.

These resources are not perfect and are subject to unverified (and perhaps outdated) user input. However, you can still collect information to help you with your search, as long as you understand that it may not be 100% accurate.

CreditBoards.com

CreditPulls Database on CreditBoards.com is a popular online source of information about credit card applications. You can use the database to find out which credit reports are likely to be obtained for your application, as well as the number of points you may need to get approved for a particular card. (Tip: Check the date of the post; there may have been changes since the data was posted.)

Access the database using the following steps:

- Visit CreditBoards.com.

- Click creditScissors options on the menu bar.

- Choose your search criteria — applicant’s state of residence, credit reporting agency (CRA), filing date, and whether the application was approved or denied.

- Click “Update”.

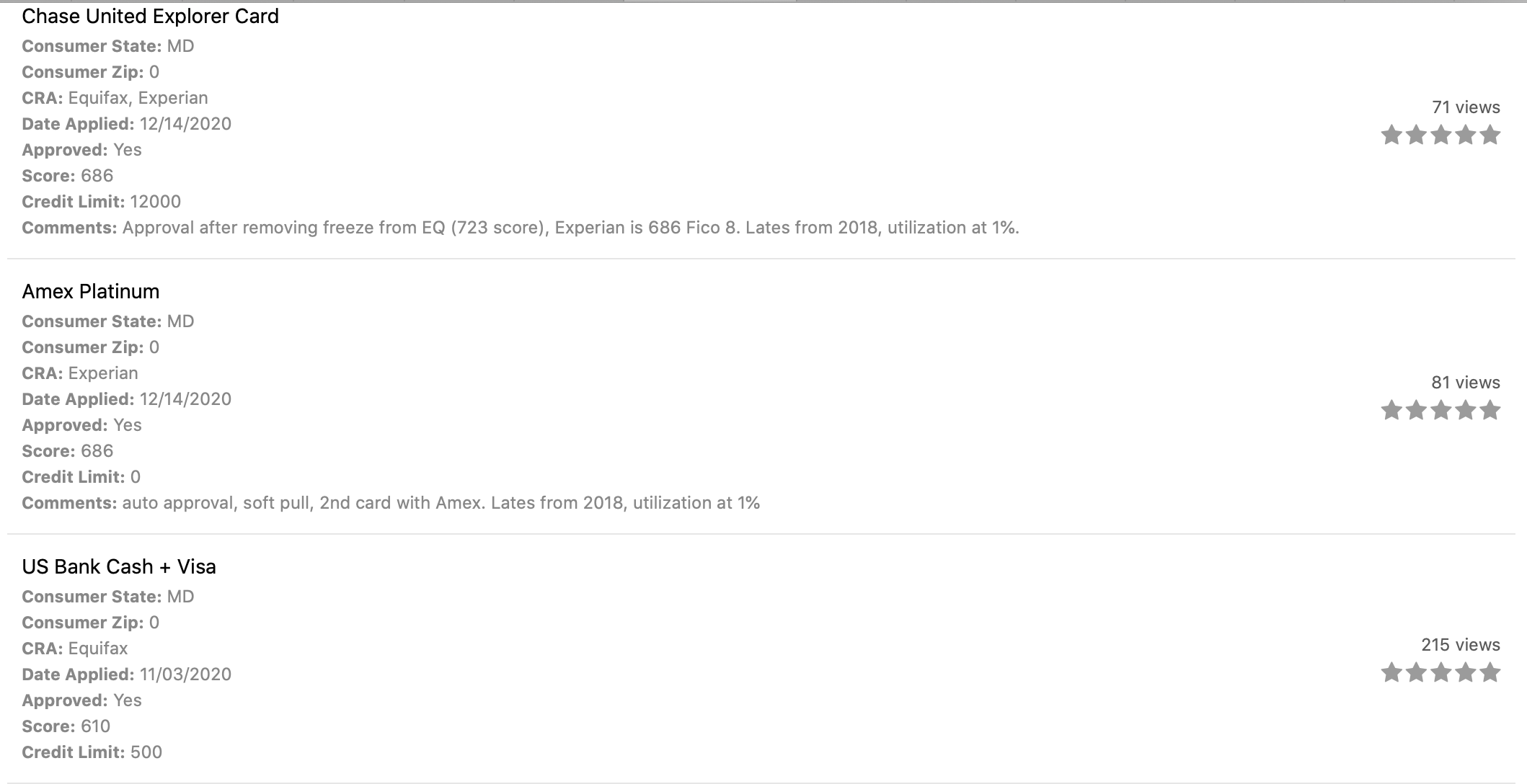

To see a broader range of card issuer options, simply enter your state and date range in the search criteria. For example, I went through and looked up data on credit draws made throughout 2020 in Maryland. Here are some results:

However, I must emphasize again that the agent that the card issuer uses to obtain the report can fluctuate between cities and even individual customers. To get the best picture possible, you should check out the site yourself and enter your own information. Even then, your application results are not guaranteed to be the same as what others have experienced.

This is really just a guide to help you make an informed guess as to where the issuer might get your data.

Related: Best credit cards for excellent credit

bottom line

When you apply for a new credit card, your issuer will get data from one of the “big three credit reporting agencies”. Because information varies from agency to agency (and therefore your score varies from agency to agency), it is important to Stay up to date on your credit score at each company.

You are permitted to receive a full credit report free of charge from each agency once a year under US law. Make sure you’re taking advantage of that to track your reports and aggregated information (even if you’re also tracking your scores through your credit card issuer’s mobile apps or other financial services).

Additional reporting by Michelle Black.